Cost of Solar Panels (Complete Guide to Financing Solar Panels)

To make it easier, we have provided a table of contents so that you can jump to what ever section you want.

- Cost of Solar Panels Breakdown

- Evolution of Residential Solar PV System Costs (2009-2017)

- Understanding the Comparative Cost of Solar Panels

- Financing Your Solar Panels

- Status Quo – Putting Off Solar For Now

- Solar Lease

- Power Purchase Agreement (PPA)

- Ownership with Outright Purchase/Solar Loan/PACE Financing

1. Cost of Solar Panels Breakdown

The cost of solar panels for your home is determined by two major cost categories: hardware and "soft costs".The hardware category includes solar panels (also called modules), inverters, racking systems, and other electrical and structural components (lovingly called "balance-of-system" or BOS hardware). The cost of solar hardware has decreased significantly in the last few years, and today, hardware costs account for about 32% of the total installation cost.

The second major cost component, the so-called "soft costs", includes labor, contractor profits, contractor overhead, permits and customer acquisition costs. All of these items add up to about 68% of the installation cost.

Fact #1: The average cost of solar panels (including all hardware and 'soft costs') in the U.S. is $2.80 per watt (2017 data).

Itemized List

| Item | Cost per watt | Legend |

|---|---|---|

| Profit | $0.34 | |

| Overhead | $0.31 | |

| Customer acquisition (Sales & Marketing) | $0.34 | |

| Permitting, Inspection, Interconnection | $0.10 | |

| Installation labor | $0.30 | |

| Sales tax on equipment | $0.09 | |

| Supply chain cost | $0.42 | |

| Electrical BOS | $0.24 | |

| Structural BOS | $0.11 | |

| Inverter | $0.19 | |

| Module | $0.35 | |

| Total | $2.80 |

Data Source: National Renewable Energy Laboratory, U.S. Solar Photovoltaic System Cost Benchmark: Q1 2017 Benchmark

2. Evolution of Residential Solar PV System Costs (2009-2017)

Since 2009, the cost of solar panels has decreased by a whopping 60%. Combined with the 30% federal tax credit, this reduction in overall installation costs has been a major catalyst for the growth of the solar industry.Intense competition and economies of scale in the solar hardware market led to plummeting prices for solar panels followed by large reductions in inverter prices and, more recently, in racking system prices. However, after years of steady decline, costs are now leveling off.

The next challenge in cost reduction is decreasing the share of "soft costs". However, cost items such as labor, profit and overhead tend to be much more "sticky" than hardware costs. Although further consolidation in the industry may bring further reductions in this category, the rate of decrease is likely to be less dramatic.

Fact #2:In the last few years, we haven't seen the dramatic price drops that we saw earlier in the decade. If you're playing the waiting game with the expectation of further cost reductions, you may be losing out on significant savings today.

| Period | Cost per watt |

|---|---|

| Q4 2009 | $6.96 |

| Q4 2010 | $6.1 |

| Q4 2011 | $4.31 |

| Q4 2012 | $3.77 |

| Q4 2013 | $3.31 |

| Q1 2015 | $3.09 |

| Q1 2017 | $2.80 |

Data Source: National Renewable Energy Laboratory, U.S. Solar Photovoltaic System Cost Benchmark: Q1 2017 Benchmark

3. Understanding the Comparative Cost of Solar Panels

Although cost per watt is a handy indicator for understanding the cost of solar panels, it should be used together with another cost metric: levelized cost.Levelized cost takes into account the location of the installation as well as the expected lifetime of the solar panels. It is generally expressed in dollars (or cents) per kWh. This is a very useful metric, as it allows us to compare the cost of solar to the status quo - your current utility rate. When the levelized cost is the same or less than the utility rate, we have "grid parity". All of these factors are important in answering the question are solar panels worth it?

We prepared some handy grid parity maps (at the bottom of the page) for you to compare the levelized cost of solar to your utility in your state or province.

Fact #3:Ultimately what really matters is how much solar power costs compared to your utility. See how your state or province compares by clicking on the map below.

4. Financing Your Solar Panels

One of the biggest disadvantages of solar power is the steep price tag that stands between homeowners and their shiny new solar panels. Although the installed price of residential solar PV systems has decreased substantially in the last five years, the initial cost is still significant for most homeowners.

One of the biggest disadvantages of solar power is the steep price tag that stands between homeowners and their shiny new solar panels. Although the installed price of residential solar PV systems has decreased substantially in the last five years, the initial cost is still significant for most homeowners.

One way to make solar energy more accessible is to decrease the upfront expenses for the consumer. There are three different paths to putting solar panels on your roof. You can lease them, you can be a solar utility customer (also known as a power purchasing agreement, or PPA), or you can purchase them (with or without a loan or PACE financing). Each of these three paths has its own advantages and disadvantages.

If you’re in Canada we tackle how to pay for your solar panels as well.“In general, I would always advise everyone to finance their solar system,” says solar industry expert Jigar Shah. “A loan is almost always the lowest cost option, but PACE financing and a PPA can also work.”

For James Hahn, CEO of My Solar Home, the role of a solar company is more than being a hardware installer.

But first, let’s talk a little about another path many homeowners choose: putting off solar and sticking with their utility.“We not only educate them on their customized personal solar energy savings plan, but provide them background on the market in general and the different finance options they have available for them to go solar ($0 down lease or $0 down purchase). By ensuring they have a complete and thorough understanding of all their available options, we empower our customers to make the best decision for their own home.”

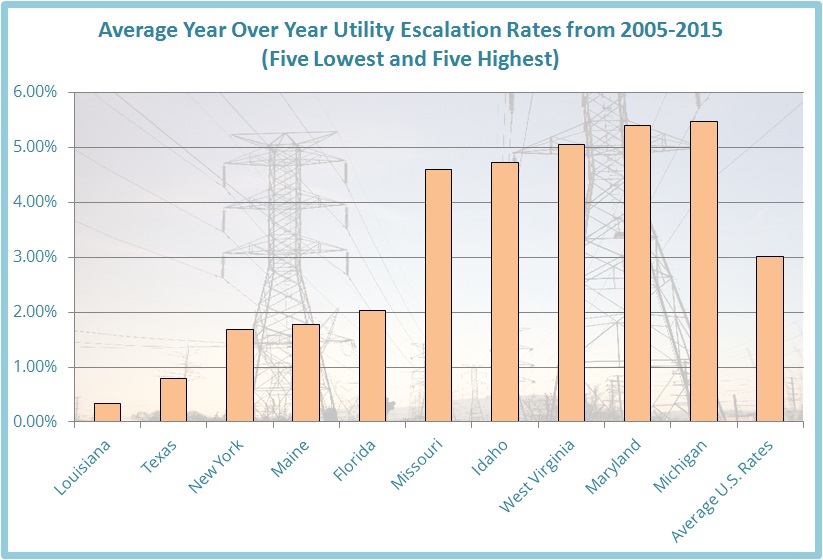

5. Status Quo – Putting Off Solar For Now

Many homeowners find the idea of getting solar panels daunting and end up doing nothing. This might be the right decision in some locations or for some particular cases, but for those of you who would do better by switching to solar, it’s important not to delay too much. If you’re unsure about whether you should stick with your utility, maybe you want to consider by how much your electricity rate has increased over the past decade. This is called the escalation rate. The average year over year escalation rate across the U.S. since 2005 was 3.01%. If you want to compare that to the average year over year rate of inflation rate in the U.S. since 2005, it was about 1.9 percent. In many states, the escalation rate for electricity has exceeded the inflation rate over the past decade.

If you’re unsure about whether you should stick with your utility, maybe you want to consider by how much your electricity rate has increased over the past decade. This is called the escalation rate. The average year over year escalation rate across the U.S. since 2005 was 3.01%. If you want to compare that to the average year over year rate of inflation rate in the U.S. since 2005, it was about 1.9 percent. In many states, the escalation rate for electricity has exceeded the inflation rate over the past decade.

Although there is variability from year to year, with some states experiencing a decrease in one year or another, the overall trend in the U.S. is increasing electricity rates. By going solar today, you protect yourself from increasing electricity rates, and the more they go up, the more you will be saving in the long run.

If sticking with the status quo doesn’t appeal to you, let’s consider your solar options.

6. Solar Lease

A solar lease can be very tempting if you live in a state with high electricity rates and/or a high electricity escalation rate over the past decade, especially when there are a number of companies offering zero-down lease options and the peace of mind that comes from someone else taking on the responsibility of maintenance for years to come.

A solar lease can be very tempting if you live in a state with high electricity rates and/or a high electricity escalation rate over the past decade, especially when there are a number of companies offering zero-down lease options and the peace of mind that comes from someone else taking on the responsibility of maintenance for years to come.

Most of us are quite familiar with the concept of a lease. An automobile lease is the prime example: instead of an all-cash purchase, we can start driving a brand new car as soon as we start making monthly lease payments. The catch, of course, is the ownership. The car doesn't belong to us; it's still the property of the leasing company, and we just have the privilege of using it. At the end of the lease term, the lease has to be renewed or the car has to be returned to the owner.

The case of a solar lease is very similar. A leasing company will pay for the installation of solar panels on your roof, and even take the responsibility for maintaining and servicing them as needed. Naturally, the ownership of the solar panels and other necessary equipment stays with the leasing company.

Your obligation as the homeowner is to make your monthly lease payments and occasionally give access to your roof for maintenance work. In most cases, there are no upfront payments for the lease, and you just start with the first regular monthly payment. This "$0 down" or "free installation" feature of the lease makes it very attractive for many homeowners, but as we'll discuss later, it may not always be the most sensible financing option when it comes to solar power for your home.

We often refer to residential solar power systems as an investment. If you own the system, it adds significant value to your home. If you are leasing, however, you are paying for the right to use somebody else's assets, not your own. Thus, the lease is not an investment on its own. However, if it frees up some cash so that you can find a better investment alternative to increase your net wealth, then the lease option can still be very useful.

In the case of a lease, you get to use all of the solar electricity you produce. Any excess can be returned to the grid for a credit and if you need extra, you purchase it from the utility at the normal retail electricity rate. However, as with any third-party ownership agreement, you will not be able to claim the federal investment tax credit (ITC) of 30% for solar installations.

With a solar lease, it is very important to look at the fine print and to consider your situation carefully. Are you planning on moving anytime soon? If so, ask about your options because a number of homeowners have run into difficulties when it was time to sell their home - not every prospective buyer is going to want to take over your solar lease.

There are other questions to consider. Is there an option to own the panels at the end of the lease term? And what is the escalation rate - in other words, by how much will your monthly payments increase every year? With a solar lease, there is generally a fixed escalation rate for the term of the agreement, so the cost of your solar electricity will go up, but because the escalation rate is fixed, you know exactly by how much it will rise, unlike with retail electricity.

7. Power Purchase Agreement (PPA)

A PPA is another third-party ownership arrangement, where you do not own the panels (and cannot claim the ITC). The solar power purchasing agreement (PPA) and the solar lease are close cousins. The biggest difference is how the monthly expenses are calculated. With a solar lease, your monthly lease payments are fixed. With a solar PPA, your monthly payments depend on how much power you generate.

A PPA is another third-party ownership arrangement, where you do not own the panels (and cannot claim the ITC). The solar power purchasing agreement (PPA) and the solar lease are close cousins. The biggest difference is how the monthly expenses are calculated. With a solar lease, your monthly lease payments are fixed. With a solar PPA, your monthly payments depend on how much power you generate.

The kilowatt-hour (kWh) rate is fixed for the year, but the actual monthly payments of your PPA will fluctuate depending on how much electricity you generate. Just like the solar lease option, you still need to keep your customer account with your traditional utility to offset low solar electricity months and to get credit when you have excess production.

Just as with a lease, you want to check the details of any PPA agreement. You should look into the escalation rate so you know by how much your kWh rate will rise over the term of the agreement. You should also understand your options at the end of the agreement, such as whether you will have the option to buy the system or not.

While this option may be very attractive because of the low, or no upfront, cost and the fact that you are unlikely to be responsible for maintenance, it is not for everyone. Like a solar lease, it is very important to consider the fine print and your particular situation.

8. Ownership with Outright Purchase/Solar Loan/PACE Financing

Just like with electronic devices, there seems to be one thing that's almost certain: the price of your panels will go down right after you buy them. The decrease in solar equipment costs in the last few years has been incredible. But there are many cost elements that are part of a solar PV installation, and the cost of the panels themselves is becoming less and less important when compared to other so-called soft costs, such as design, permitting and customer acquisition.Outright Purchase

An outright solar purchase generally offers you the best return on your investment (ROI) because as the system owner, you can take advantage of the generous ITC available at the federal level, in addition to any available U.S.state or Canadian provincial incentives. Moreover, once you pay off your panels, your solar electricity is "free" for the remaining lifetime of your panels (which can last more than 25 years) with no risk of cost escalation.This doesn’t mean that you can say goodbye to your utility (unless you’re completely off the grid). In most cases, you will still be keeping your account with the utility (and paying the fixed charges necessary to keep your account active), so that you can get extra power when you need it or get credit for the excess when you don’t need it.

As the owner of the system, you will be responsible for any required maintenance, which is generally minimal most years, but will eventually include replacement of the inverter(s).

Solar Loan

Most people cannot afford an outright purchase of their solar system, so another option is the solar loan, many of which come with a zero down-payment option.While you will have to pay interest on the loan, the interest rate is fixed for the duration of the loan and there is no escalation rate. Moreover, a solar loan can enable you to claim the federal income tax credit (ITC), while minimizing the initial investment required.“Homeowners are looking for an easy, affordable and flexible alternative to solar leasing,” explains Stephanie Bonini, Senior Regional Sales Manager at Sungage Financial.

It’s important to understand, however, that the ITC is a deferred payment that comes to you after filing your taxes. In order to make the solar loan option even more affordable, some loan providers such as Sungage Financial offer a 0% APR tax credit loan to cover the ITC amount until the payment is received (generally with a loan term of 12 months).

Unlike with a lease or PPA, you will be responsible for the maintenance of your system and the occasional equipment replacement. As solar loan providers are working with installers that they know, an added benefit of choosing a solar loan over an outright purchase is that you may have more recourse should an issue arise with the performance of your panels. As Jigar Shah points out, “the reason not to pay cash is because solar systems will have maintenance issues and it is important to work with a financing provider who is incentivized to make sure that your solar installer maintains your system properly - the loan is how you have leverage over making sure your system is always working.” Some solar loan providers, such as Sungage Financial, require installers to include a minimum 10 Year Workmanship Warranty on the equipment they are installing on the homeowner's roof. With a loan, just as with a lease or PPA, it still important to look at the fine-print. In particular, you should understand if there are any dealer/loan fees that must be paid at the outset. Generally, the lower the interest rate, the higher the initial fees. Stephanie Bonini from Sungage Financial offers these words of advice:“The tax credit loan is essentially a free loan for the homeowner to offset the deferred receipt of the federal tax credit,” according to Bonini.

Homeowners should also be looking at their contract to understand if there are any pre-payment penalties.“As with any loans, homeowners should always educate themselves on the interest rates and fees of their solar financing options. For example, very low interest rates that seem ‘too good to be true’ are often a result of rate ‘buy-downs,’ which are basically tactics by the lender to keep interest rates artificially low. Those low rates are ultimately still paid for by the homeowner via inflated system costs and/or other hidden fees.”

At first glance, many solar leases may seem less expensive, but more and more solar loan options remove the initial upfront costs, making the solar loan more attractive.“Homeowners are looking for solar loans they can pay off whenever they want—without having to worry about pre-payment penalties,” explains Bonini.

And at the end of the loan term, you own the panels, unlike with a solar lease.“In New Jersey, for example, a 15-year Sungage Solar Loan costs about the same per month as a 20 -25-year solar lease,” according to Bonini.

PACE Financing

Another mechanism for financing solar panels is PACE Financing. PACE stands for Property-Assessed Clean Energy. The PACE programs allow homeowners to implement a number of energy efficiency and renewable energy improvements on their private property.Energy.gov explains PACE financing like this:

Rommel Dingle, Sales Manager at Golden Gate Power in San Francisco believes that PACE financing offers a number of advantages.“Property owners who voluntarily choose to participate in a PACE program repay their improvement costs over a set time period—typically 10 to 20 years—through property assessments, which are secured by the property itself and paid as an addition to the owners' property tax bills. Nonpayment generally results in the same set of repercussions as the failure to pay any other portion of a property tax bill.”

With PACE financing, because the debt is tied to the property as opposed to the homeowner, the re-payment obligation transfers with the property.“It isn’t limited to solar projects, and can include insulation, water efficiency (including synthetic turf), roofing projects, windows and doors, air conditioners (including new installations), and furnaces,” says Dingle. Moreover, homeowners can take advantage of the Federal ITC and “there are no monthly payments (unless property tax is impounded with the mortgage); payments are paid in the frequency matching property tax payments.”

Many homeowners are reluctant to make property improvements if they think they may sell soon and not be able to recoup their initial investment.“This is an important consideration for a homeowner when it comes to the sale of their property,” according to Dingle.

However, homeowners thinking of using PACE financing should be aware of a potential limitation, that certain criteria must be met, with regard to the home improvements.

“Products other than solar that are funded by PACE will need to meet certain energy efficiency benchmarks,” Dingle explains. “For example, some solar projects require the installation of a new roof. If PACE is to fund the entire project, the new roof must meet cool roof benchmarks and can increase the cost of a project significantly.”

A Few More Words on Ownership

There are other types of financing available that you might be considering, such as personal loans, home-equity loans or home-equity line of credit. These are especially relevant in Canada where there is no federal investment tax credit. If you are considering these options, it’s good to keep in mind a few words of advice from Stephanie Bonini at Sungage Financial:A big advantage of ownership: there is no "20-year lease term". In all likelihood, your solar panels will continue to keep on ticking after 20 years (25 years on average). Each additional year of service will be a bonus and increase the financial appeal of ownership. Yes, there is some maintenance work to do, and the occasional equipment replacement. But compared to your car, for example, these costs are going to be less frequent. Another major advantage of owning your solar system is that they increase the market value of your home.“When compared to other traditional loan options, the advantage of solar loans is financing features that are specifically designed for the purchase of solar arrays, such as a built-in, ‘same as cash’ tax credit options. Ideally, the solar loan provider would also have an in-depth understanding of the solar industry and strong working relationships with installers. Just as a home mortgage is very different from a car loan, a solar loan is very different from a traditional home improvement loan.”

Grid Parity Maps for the United States, Canada and Australia

UNITED STATES

Cost of residential solar power is less than the average utility rate in all U.S. states after the federal tax credit. Learn more.

CANADA

A number of provinces are offering solar incentives, making solar panels in Canada more attractive. Learn more.

Latest Update: December 2018

Spread the solar goodness: please share this resource with your friends and family.